NVIDIA II (2006-2022)

Machines learned how to learn. And they learned it... on Nvidia.

By 2012, NVIDIA was on a decade-long road to nowhere. Or so most rational observers of the company thought. CEO Jensen Huang was plowing all the cash from the company’s gaming business into building a highly speculative platform with few clear use cases and no obviously large market opportunity. And then... a miracle happened. A miracle that led not only to Nvidia becoming the 8th largest market cap company in the world, but also nearly every internet and technology innovation that’s happened in the decade since. Machines learned how to learn. And they learned it... on Nvidia.

Company Overview

Company Name: NVIDIA Corporation

Year Founded: 1993

Headquarters Location: Santa Clara, California

Core business and significance: NVIDIA is one of the most valuable companies in the world. NVIDIA’s core business is designing and manufacturing graphics processing units (GPUs) and related software, evolving from gaming-focused graphics cards to a full-stack platform for accelerated computing, including machine learning (ML), data centers, automotive, and digital twins.

History and Facts

Timeline

1999: NVIDIA ships the GeForce 256, the first consumer GPU, establishing dominance in gaming graphics.

2000–2001: Releases GeForce 2 and GeForce 3, introducing programmable shaders, accelerating graphics innovation.

2006: NVIDIA begins developing CUDA, a platform for general-purpose GPU computing, targeting scientific and enterprise markets.

2008: Launches Tegra chip for mobile devices; stock drops 80% after missing earnings, reflecting gaming focus lapse.

2011: Another earnings miss leads to a 50% stock drawdown as CUDA investments remain unproven.

2012: AlexNet, a CUDA-based deep learning model, wins ImageNet competition, sparking AI revolution and validating CUDA.

2013: NVIDIA researchers publish a paper enabling efficient deep neural networks (cuDNN), boosting AI accessibility.

2018: Crypto mining demand surges then crashes, causing a 50% stock drawdown; NVIDIA restricts consumer GPUs in data centers.

2020: Acquires Mellanox for $7 billion, enhancing data center networking capabilities.

2022: NVIDIA targets a $1 trillion market opportunity, with data center revenue rivaling gaming at $10.5 billion.

Narrative

NVIDIA’s journey from 2006 to 2022 is a saga of audacious bets and serendipitous breakthroughs.

By 2006, NVIDIA had conquered the gaming market, riding a wave of programmable shaders and six-month chip cycles that left competitors like ATI trailing. Its GeForce cards powered immersive gaming experiences, and a lucrative Microsoft partnership for the Xbox solidified its $5–$6 billion market cap. Yet, Jensen, restless with gaming’s limits, saw GPUs as more than pixel-pushers.

Inspired by an apocryphal tale of a Stanford researcher accelerating quantum chemistry models on GeForce cards, he envisioned GPUs revolutionizing general-purpose computing. This led to CUDA’s development in 2006—a platform to make GPUs accessible for non-graphics tasks like scientific simulations and drug discovery. Ben and David marvel at the scale of this gamble, likening it to building an iPhone-sized ecosystem without a clear market, as Jensen poured gaming profits into a speculative venture Wall Street largely ignored.

The late 2000s tested NVIDIA’s resolve. The 2008 financial crisis and a focus on CUDA over gaming led to an earnings miss, slashing the stock by 80% from its $20 billion peak. Ben and David paint a vivid picture of a company “in the penalty box,” with headlines questioning NVIDIA’s survival as AMD’s acquisition of ATI bolstered a gaming-focused rival. Jensen’s foray into mobile with the Tegra chip, powering devices like the Microsoft Zune HD and Tesla’s early touchscreens, was a misstep that leveraged little of NVIDIA’s core strengths. By 2011, another earnings miss and a 50% stock drop underscored the market’s skepticism of CUDA’s unproven potential. Yet, as David notes, “Jensen didn’t flinch.” His mantra—“if we don’t build it, they can’t come”—drove relentless investment in CUDA, a platform that, by 2012, employed 1,100 specialized engineers. Ben and David’s tone shifts to awe as they describe the 2012 AlexNet breakthrough, where a CUDA-based neural network crushed the ImageNet competition, proving GPUs’ prowess in deep learning. This “big bang moment for AI,” as David calls it, validated Jensen’s vision, aligning NVIDIA with an exploding AI market.

From 2012 to 2022, NVIDIA capitalized on this miracle. The 2013 cuDNN library made deep learning accessible, fueling adoption by tech giants like Google and Facebook. Ben and David highlight NVIDIA’s pivot to enterprise data centers, where high-margin A100 and H100 GPUs, priced at $20,000–$30,000, powered AI training for customers like Tesla, who spent $50–$100 million on NVIDIA hardware. The 2020 Mellanox acquisition enabled high-bandwidth data center solutions, introducing the DPU (data processing unit) alongside CPUs and GPUs. By 2022, NVIDIA’s data center segment matched gaming at $10.5 billion, with a 66% gross margin reflecting its platform dominance. Ben and David’s enthusiasm peaks as they discuss NVIDIA’s Omniverse, a digital twin platform for enterprise simulations, and its automotive ambitions, though they note the latter’s modest $1 billion revenue. Despite a failed $40 billion Arm acquisition in 2022, NVIDIA’s 60% annual growth and $27 billion in revenue cemented its status as the eighth-largest company by market cap. Ben and David conclude with a nod to Jensen’s trillion-dollar market pitch, blending admiration for his foresight with cautious optimism about sustaining such lofty valuations.

Notable Facts

CUDA’s Scale: By 2022, CUDA supports 3 million developers and 450 SDKs, enabling applications from AI to robotics, all free but proprietary to NVIDIA hardware.

Gaming Innovation: NVIDIA’s RTX cards introduced real-time ray tracing and DLSS (deep learning super sampling), blending AI with gaming for high-resolution, high-frame-rate visuals.

Crypto Impact: NVIDIA restricted consumer GPUs in data centers and launched dedicated crypto mining cards to stabilize gaming supply and boost margins.

Mellanox Acquisition: The $7 billion deal enhanced NVIDIA’s data center dominance, enabling high-bandwidth DPUs for AI workloads.

Failed Arm Bid: NVIDIA’s $40 billion attempt to acquire Arm in 2020–2022 was abandoned due to regulatory concerns, but it spurred the Grace CPU for data centers.

Financial / User Metrics

Revenue (2021): $27 billion, with 60% year-over-year growth.

Data Center Revenue: $10.5 billion, nearly equaling gaming’s $10.5 billion, up from $3 billion two years prior.

Gaming Revenue: $10.5 billion, driven by RTX cards and crypto mining demand.

Automotive Revenue: ~$1 billion, flat and small relative to other segments.

Gross Margin: 66%, up from 30% in 1999 and 50% in 2014, reflecting high-margin data center solutions.

Operating Margin: 37%, surpassing Apple’s, driven by fabless model and software bundling.

Free Cash Flow: $8 billion annually, with $21 billion cash on hand.

Market Cap: ~$500 billion, eighth globally, with a price-to-sales ratio 3x Apple’s.

CapEx: $1 billion annually, low compared to Apple ($10 billion) or TSMC ($30 billion).

Developers: 3 million registered CUDA developers.

Data not provided in episode: Specific user metrics (e.g., active users per segment) or detailed automotive revenue breakdown.

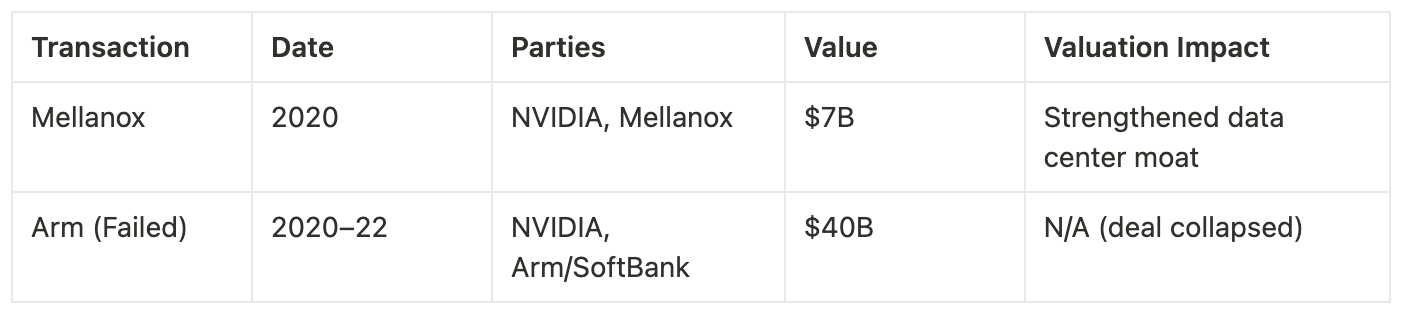

Transaction

No major acquisition, IPO, or financial event is the primary focus of this episode, which instead chronicles NVIDIA’s strategic evolution from 2006 to 2022. Ben and David mention two transactions briefly:

Mellanox Acquisition (2020): NVIDIA acquired Mellanox, an Israeli data center networking company, for $7B. This bolstered its data center capabilities, enabling high-bandwidth, low-latency interconnects like NVLink. David: “It lets them treat the data center as the black box.”

Failed Arm Acquisition (2020–2022): NVIDIA attempted to buy Arm for $40B to integrate its CPU architecture into data centers. Regulatory pressure killed the deal, as competitors feared NVIDIA would restrict Arm’s licensing. Ben: “They were talking about it like it was done, then poof.”

The Mellanox deal’s immediate impact was enhanced data center offerings, introducing the DPU (data processing unit) alongside CPUs and GPUs, boosting gross margins. Long-term, it positions NVIDIA to dominate AI infrastructure, as enterprises buy “solutions, not cards,” per David. The Arm failure avoided regulatory entanglements but limited NVIDIA’s CPU ambitions, though the Grace CPU launch in 2022 mitigates this. Both moves reflect Jensen’s strategy to own the compute stack, with Mellanox proving more transformative than the aborted Arm deal.

Grading

Ben and David don’t assign a formal grade for NVIDIA’s performance from 2006 to 2022, instead framing its success through a narrative of bold bets, resilience, and market creation. However, their enthusiasm suggests an implied A+ for Jensen Huang’s vision and execution, tempered by market volatility and investor skepticism. David calls NVIDIA “a generational company,” celebrating its survival through four near-death experiences, including the 2008 stock crash and 2011 earnings miss. Ben likens CUDA’s development to “Apple’s iPhone gamble,” emphasizing its transformative impact. They evaluate NVIDIA’s broader trajectory as a platform company, not a specific transaction, highlighting its shift from gaming to AI dominance.

No acquisition categories (e.g., talent, technology) are explicitly outlined, as the episode focuses on organic growth via CUDA and market shifts like AlexNet. Ben and David do, however, discuss a bull case and bear case for NVIDIA’s future, particularly from an investor perspective given its $500B market cap and high valuation in 2022. These cases provide a lens to grade NVIDIA’s potential outcomes:

Bull Case: The bull case hinges on NVIDIA maintaining its AI dominance and capturing new markets. Ben outlines that investors must believe NVIDIA’s data center segment, growing 75% year-over-year, will “continue to own that market.” This requires sustained innovation, integrating lessons from competitors like Cerebras, and redefining GPUs to handle diverse workloads. David adds that real-world AI applications—autonomous vehicles, robotics, and the Omniverse—must materialize as “enormous markets” where NVIDIA is a key player. Ben notes Jensen’s pitch of a “$100T opportunity” with NVIDIA capturing 1%, though David calls it “squishy.” Continued digital AI growth, especially in advertising, supports this, as Ben quotes Marc Andreessen: “Every deep learning company builds on NVIDIA.” An A+ outcome would see NVIDIA sustain 60% revenue growth, leveraging its 3M developers and 66% gross margins to dominate both digital and physical AI, justifying its valuation. David: “It’s like betting on the internet.”

Bear Case: The bear case questions NVIDIA’s growth sustainability and competitive moat. David suggests a failure scenario where “amazing growth was a pandemic pull-forward,” akin to Zoom or Peloton, though he doubts it’s that severe. Ben highlights competition risks: AMD in gaming, where both support high-end games, and startups like Cerebras or Graphcore in data centers, which could disrupt with specialized AI chips. David emphasizes the threat from big customers (Google, Tesla, Amazon) designing in-house silicon, like Google’s TPUs or Tesla’s Dojo chips, to bypass NVIDIA’s high-margin hardware. Ben: “If you’re Google, your customer is only yourself, constrained by Google Cloud’s share.” A failure case would see NVIDIA’s stock falter if growth slows or competitors erode its ecosystem, as Ben warns: “It’s easy to imagine a failure case for the stock if people lose faith.” This suggests a C or lower grade if NVIDIA’s valuation collapses without new markets materializing.

Analytically, NVIDIA’s 2006–2022 performance is stellar: $27B revenue, 60% growth, and a $500B market cap. Ben notes skepticism lingered until 2016, with analysts dismissing Jensen’s neural network focus as “crazy.” The company’s pivot to AI, capturing data center value, earns high marks, but stock volatility (e.g., 2018 crypto crash) reflects execution risks. The bull case supports an A+ grade if NVIDIA sustains its platform moat, while the bear case warns of a potential C if competitors or market shifts disrupt its trajectory. This ties to NVIDIA’s strategy of building a proprietary ecosystem, outlasting doubters to lead AI compute, as David sums up: “Jensen endured the pain.”

Tech Trends

Ben and David identify three technological waves shaping NVIDIA’s success:

Deep Learning/AI: The 2012 AlexNet breakthrough, using CUDA, proved GPUs’ superiority for neural networks. David: “This was the big bang moment for AI.” CUDA’s parallel architecture enabled computationally intensive deep learning, powering applications from image recognition to digital advertising. Ben: “It’s like grains of sand on Earth for one model.”

Accelerated Computing: NVIDIA redefined GPUs as general-purpose platforms, offloading tasks from CPUs. Ben: “Wherever there’s a CPU, there’s an opportunity to accelerate it.” This trend spans gaming (DLSS), data centers (H100), and scientific computing, with CUDA as the linchpin.

Digital Twins/Omniverse: NVIDIA’s Omniverse platform creates virtual simulations for enterprises, like Earth 2 for climate modeling. David: “This is the enterprise Metaverse, not for humans but for applications.” It leverages AI and GPU power for real-world testing, reducing physical prototyping costs.

These trends interlock with NVIDIA’s playbook. Deep learning fueled data center growth, requiring CUDA’s ecosystem (Playbook: proprietary platform). Accelerated computing underpins NVIDIA’s hardware-software integration (Powers: scale economies), while Omniverse extends this to new markets (Playbook: mission expansion). Risks include competitors like Cerebras building specialized AI chips, but NVIDIA’s developer lock-in and cross-cloud availability (AWS, Azure) maintain its edge. Ben: “They’ve got 3 million developers—good luck competing with that.”

Playbook

Ben and David distill five strategic themes from NVIDIA’s 2006–2022 journey:

Picks and Shovels in a Gold Rush: NVIDIA capitalized on the AI boom by selling GPUs and CUDA, not chasing end applications. David: “You want to invest in whoever’s selling the picks and shovels.” This ensured NVIDIA profited regardless of which AI startups succeeded, as Marc Andreessen noted in 2016: “Every deep learning company builds on NVIDIA.”

Mission Expansion: NVIDIA evolved from gaming to accelerated computing for all workloads. Ben: “From enabling graphics as storytelling to accelerating every CPU.” This flexibility opened trillion-dollar markets, though Jensen’s “1% of $100T” claim is “squishy,” per David.

Enduring Pain: NVIDIA survived multiple crises (2008, 2011, 2018 stock drops) by sticking to Jensen’s vision. David: “They should have died four times, but Jensen just sat there and endured.” This resilience built a platform that competitors can’t replicate overnight.

Proprietary Ecosystem: CUDA’s free but closed-source model locks developers into NVIDIA hardware. Ben: “It’s like iOS—you can’t run it elsewhere.” This creates switching costs, amplifying margins as enterprises buy solutions, not components.

Capital Efficiency: NVIDIA’s fabless model, leveraging TSMC, keeps CapEx low at $1B annually versus $25B for Google. Ben: “It’s like a software business.” This fuels high margins (37% operating) and cash reserves ($21B), enabling bold bets like Mellanox.

These strategies connect to Tech Trends (AI and Omniverse rely on CUDA’s ecosystem) and Powers (scale economies from 3M developers). They position NVIDIA for growth in data centers and automotive, though Ben warns of segmentation challenges if software licensing cannibalizes hardware sales. David counters: “They’ll wall off segments like Apple does.”

Powers

The most relevant of Hamilton Helmer’s 7 Powers is Scale Economies, implied by Ben and David’s focus on CUDA’s vast ecosystem and NVIDIA’s market dominance. CUDA’s development, costing billions and employing 1,100+ specialists, is amortized over 3 million developers and $27B in revenue. David: “You needed an enormous market to justify the CapEx.” This scale deters competitors, as replicating CUDA’s 450 SDKs and developer base is daunting. Ben: “Very few players have the capital and market to make this investment.”

Switching Costs also apply, as CUDA’s proprietary nature locks developers into NVIDIA hardware. Ben: “If you boot out NVIDIA, you’re booting out CUDA.” This reinforces pricing power, yielding 66% gross margins. The ecosystem acts as a platform, akin to Apple’s iOS, tying into the Playbook’s proprietary strategy and Tech Trends’ AI dominance. While Cornered Resource (CUDA’s exclusivity) is arguable, scale economies dominate, enabling NVIDIA to outspend rivals and maintain its AI compute moat.

Carveouts

David’s Carveout: Memory’s Legion, a collection of short stories from The Expanse series. David: “They paint glimpses into corners and characters you don’t question otherwise.” He enjoys its standalone appeal and depth for fans, having prioritized reading it despite a newborn and Acquired duties.

Ben’s Carveout: Sony RX100 point-and-shoot camera. Ben: “It’s nice to have a real camera again.” Bought for an Altimeter episode, it proved ideal at Disneyland, offering mirrorless-quality images with a zoom lens, fitting in a pocket unlike bulkier DSLRs.

Additional Notes

Episode Metadata:

Number: Season 10, Episode 6

Title: Nvidia Part II: The Machine Learning Company (2006–2022)

Duration: 2:11:16

Release Date: April 20, 2022

Recording Date: Not specified, but likely early April 2022 given GTC references.

Sourced from Acquired’s website and Apple Podcasts.

Miscellaneous Insights:

The episode emphasizes Jensen Huang’s visionary leadership, with Ben and David portraying him as a rare CEO willing to endure decade-long skepticism. David: “He’s like, I’m willing to sit here and take the pain.”

The Asianometry YouTube channel is credited for driver insights, reflecting listener Jeremy’s contribution via Slack.

Ben and David’s excitement is palpable, with tangents on ray tracing, DLSS, and floorplanning, showcasing their nerdy enthusiasm.

Contradictions:

The episode claims NVIDIA’s H100 is the first 4nm chip, but web searches confirm TSMC’s 4nm process was used by others (e.g., MediaTek) earlier. This overstates NVIDIA’s lead but aligns with Jensen’s hype.

Crypto mining’s impact is described as unpredictable, but NVIDIA’s 2018 earnings reports (per Yahoo Finance) show clear mining revenue spikes, suggesting some visibility.

Related Episodes:

Nvidia Part I: The GPU Company (1993–2006) (S10E5, 3/27/2022)

Nvidia Part III: The Dawn of the AI Era (2022–2023) (S13E3, 9/5/2023)

TSMC (S9E3, 9/6/2021)